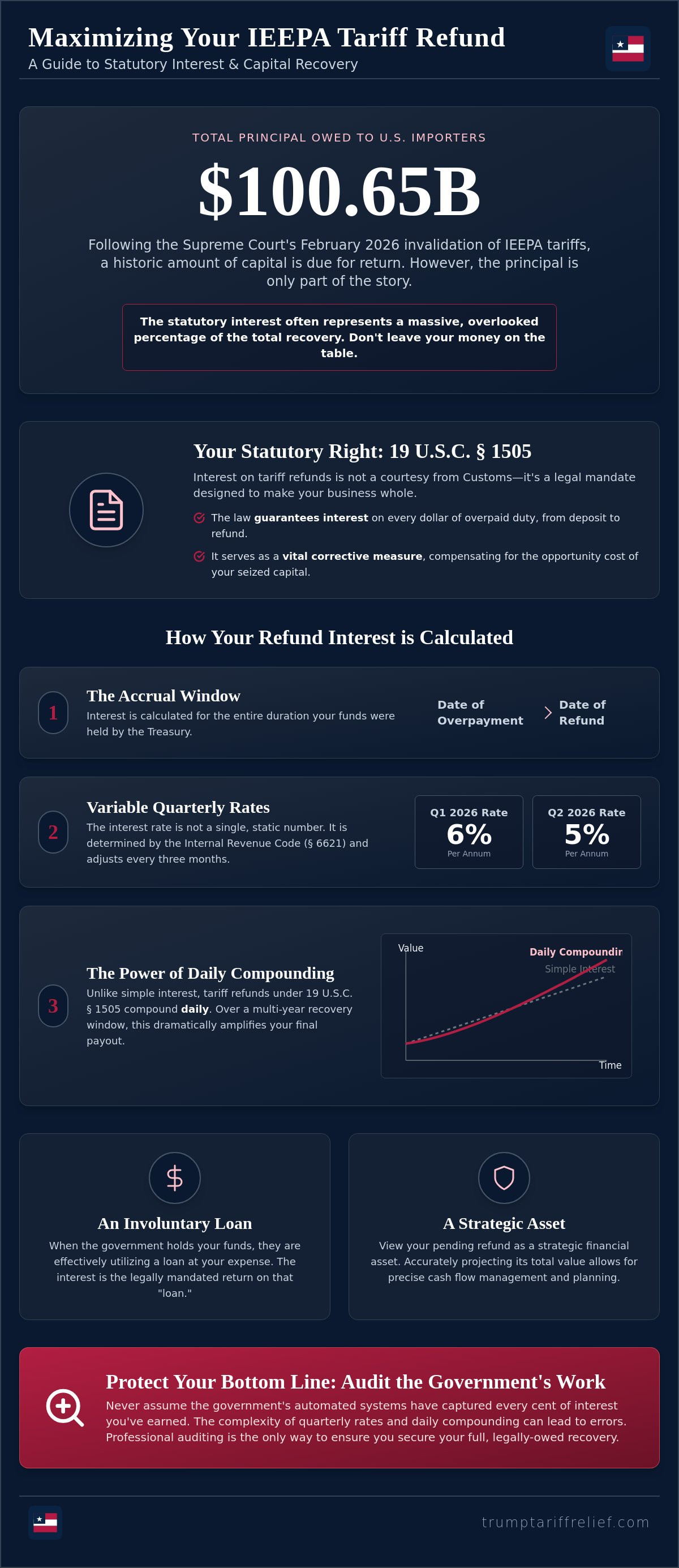

The U.S. government still owes importers approximately $100.65 billion following the Supreme Court's February 2026 invalidation of IEEPA tariffs. While the principal refund is significant, the statutory interest often represents a massive percentage of the total recovery that many businesses leave on the table. You're likely concerned that a standard check from Customs and Border Protection won't reflect the true "all-in" value of your claim. Understanding the exact mechanics of how interest is calculated on tariff refunds is the only way to ensure the government doesn't underpay what it legally owes your firm.

This article provides the precise statutory formulas and current interest rates needed to maximize your IEEPA recovery. You'll discover how the 5% to 6% quarterly rates for 2026 apply to your specific corporate structure and why daily compounding under 19 U.S.C. § 1505 can significantly boost your final payout. We'll walk through the accrual period from the date of your initial duty deposit to the moment of refund; giving you the confidence to audit your recovery and reclaim your capital with total precision.

Key Takeaways

- Reclaim what's yours by mastering the statutory requirements of 19 U.S.C. § 1505, which guarantees interest on every dollar of overpaid duty.

- Gain a competitive edge by learning exactly how interest is calculated on tariff refunds using the specific quarterly rates set by the Internal Revenue Code.

- Uncover the power of daily compounding and the 'Midpoint Date' shortcut to accurately project the total value of your recovery.

- View your pending refund as a strategic asset, treating the government’s delay as an involuntary loan with a mandated return.

- Protect your bottom line by auditing the government's work; don't assume their automated systems have captured every cent of interest you've earned.

The Statutory Right to Interest on Tariff Refunds

When the government collects excessive duties, it isn't just an administrative error; it's a temporary seizure of your working capital. Federal law recognizes that returning only the principal amount is insufficient to "make whole" a business that has been deprived of its funds. This is why interest isn't a courtesy extended by U.S. Customs and Border Protection (CBP). It's a statutory mandate designed to restore the financial position you would've held had the unlawful tariffs never been applied.

For IEEPA-related claims, where billions were collected under authority later found unconstitutional, interest serves as a vital corrective measure. It compensates for the opportunity cost of that capital. If your business had those funds, you could've invested them in expansion, inventory, or research. Instead, the money sat in the Treasury. Understanding exactly how interest is calculated on tariff refunds allows your finance team to project accurate cash flow from these pending claims rather than simply waiting for a check of an unknown amount.

The federal government uses specific logic for how interest is calculated on these overpayments. While many commercial loans utilize simple interest, tariff refunds under 19 U.S.C. § 1505 are compounded daily. This nuance is critical. Over a multi-year recovery window typical of IEEPA cases, daily compounding can add thousands or even millions to a final payout compared to simple interest models. It turns a standard refund into a significant capital recovery event.

Understanding 19 U.S.C. § 1505

19 U.S.C. § 1505 serves as the definitive statutory foundation that requires the government to pay interest on any overpayment of duties, fees, or taxes from the date of deposit to the date of refund. When duties are deemed "excessive" because a tariff is invalidated or an entry is liquidated at a lower rate, the government's obligation to return that capital is absolute. This statute applies directly to the massive IEEPA refund claims, ensuring that importers are compensated for the entire duration their funds were held by the Treasury.

The Accrual Window: From Payment to Liquidation

The timeline for your recovery is precise. Interest begins accruing on the "Date of Overpayment," which is the date you deposited the duties with CBP. It continues until the "Date of Refund," typically the day the Treasury issues the check or electronic transfer. Because the IEEPA refund process involves complex legal precedents and administrative hurdles, the window between payment and refund is often several years. Paradoxically, these long processing times work in your favor regarding the total payout. The longer the government holds your money, the more the daily compounding effect amplifies your "all-in" recovery amount. Identifying these dates for every entry is the first step in auditing your total claim value.

The Mechanics of Interest Rates: How Percentages are Determined

The interest rate applied to your refund isn't a static number. It's a moving target that shifts every three months based on broader economic conditions. Because IEEPA claims often span several years, your total recovery isn't calculated using a single percentage. Instead, the government applies a series of quarterly rates that correspond to the period they held your capital. Understanding how interest is calculated on tariff refunds requires a look at the Internal Revenue Code, specifically Section 6621, which dictates the rates U.S. Customs and Border Protection must use.

These rates are designed to reflect the "time value" of money. When the government holds your funds, they're essentially utilizing a low-interest loan at your expense. The quarterly adjustments ensure the compensation stays relevant to the market. For instance, in the first quarter of 2026, the corporate refund rate was 6% per annum. By the second quarter of 2026, that rate adjusted to 5%. If your claim covers both periods, the calculation must be segmented to reflect these changes accurately. This complexity is why many businesses inadvertently accept lower payouts than they're legally owed.

The Federal Short-Term Rate (AFR) Explained

The anchor for all trade-related interest is the Federal Short-Term Rate, also known as the Applicable Federal Rate (AFR). The Treasury Department determines this rate every quarter by averaging the market yields from outstanding marketable obligations of the United States. This baseline is then used to establish the Quarterly IRS Interest Rates for Customs Duties. For most corporate importers, the formula is the AFR plus two percentage points. Tracking these historical shifts is the only way to build a reliable estimate for older IEEPA entries that have been pending since the initial tariffs were imposed.

Corporate vs. Non-Corporate Rate Differentials

Your business structure directly impacts your recovery bottom line. The government pays a higher interest rate to non-corporate entities compared to corporations. As of the second quarter of 2026, non-corporate importers receive 6% per annum, while corporations receive 5%. Additionally, for large corporate overpayments exceeding $10,000, the rate can drop further to the AFR plus only 0.5%. These differentials make entity identification a critical step in the auditing process. If your recovery isn't segmented by these specific rules, you're likely leaving money on the table. You can see how these variables impact your specific claim by reviewing our recovery process overview. Precision in these early stages prevents the government from underpaying the interest portion of your claim.

Compound Interest and the 'Midpoint Date' Calculation

While the quarterly interest rate provides the baseline, the real engine of your recovery is daily compounding. Unlike standard commercial interest that might calculate monthly or annually, federal law requires a more aggressive accumulation of value. This ensures that the capital the government held isn't just returned, but returned with the full economic weight of its time away from your balance sheet. Understanding how interest is calculated on tariff refunds means looking past the headline rate and into the daily math that turns a standard refund into a high-yield recovery.

The "snowball effect" of daily compounding is particularly potent for IEEPA claims. Because many of these entries have been pending for several years, the interest on the interest becomes a significant portion of the total payout. For an importer with $10 million in overpaid duties, a 6% annual rate compounded daily results in a higher effective yield than simple interest. Over a three-year window, this discrepancy can amount to hundreds of thousands of dollars. If your recovery assessment doesn't account for this daily reset, you're essentially giving the government a discount on the money they took from you.

The Daily Compounding Formula

Interest on tariff refunds is compounded daily per 26 U.S.C. § 6622, a statutory requirement that forces the Treasury to add earned interest back into the principal balance every 24 hours. The calculation uses three primary variables: the principal amount of overpaid duty, the applicable quarterly rate, and the exact number of days (using a 365-day year) since the deposit. By applying the formula [Principal * (1 + (Rate / 365))^Days], CBP's systems determine your "all-in" value. Even a small error in the "Days" variable can trigger a cascading underpayment across your entire entry portfolio.

Simplifying the Midpoint Date for Importers

CBP often utilizes a "Midpoint Date" for aggregate claims, such as those filed through the Reconciliation prototype, to avoid the administrative burden of entry-by-entry calculations. This date is exactly halfway between the first and last overpayment dates in a specific group. While this simplifies the process, it's a double-edged sword. If your largest duty payments were made early in the cycle, a midpoint calculation might actually result in a lower total interest payout than an entry-by-entry audit. Many businesses don't realize they can challenge these simplified calculations. You can learn more about these nuances in our frequently asked questions. Professional auditing ensures that the method chosen—whether midpoint or entry-specific—actually maximizes your capital recovery rather than just easing the government's workload.

Strategic Impact: Interest as a Capital Recovery Tool

Smart finance teams don't view interest as a mere bonus on top of a refund. They recognize it as a high-yield financial instrument. Because the government has held your capital for years, the statutory interest mandated by law serves as a vital tool for restoring your company’s liquidity. When you analyze how interest is calculated on tariff refunds, it becomes clear that these payouts are often more lucrative than traditional low-risk investment vehicles available to corporate treasuries. Reclaiming this capital allows you to pivot from a defensive financial posture to an offensive one, reinvesting recovered funds directly back into your supply chain or R&D initiatives.

The financial significance of these payments cannot be overstated for large-scale importers. For a claim that has been pending since the height of the trade disputes, the interest component can represent 15% to 20% of the total "all-in" recovery. This isn't just "extra" money; it's the recovery of the time-value of your capital. It compensates for the missed opportunities, the financing costs, and the administrative burden your business shouldered while these funds were locked away in the Treasury's accounts.

The Involuntary Loan Narrative

Importers should frame their pending refunds as an involuntary loan to the government. You've essentially provided the Treasury with interest-bearing liquidity at a time when capital was expensive. As of the second quarter of 2026, the government is paying 5% per annum for corporate overpayments and 6% for non-corporate entities. These rates often outperform standard corporate savings vehicles or short-term money market accounts. By understanding the IEEPA Explained legal framework, you can see exactly why these funds were tied up and why the government is now legally obligated to pay a premium to return them.

Boosting Total ROI on Recovery Efforts

Viewing recovery through the lens of Return on Investment (ROI) changes the priority of a tariff audit. Because interest is compounded daily, the total value of your claim grows every 24 hours. This growth often covers the entire cost of the recovery effort itself. In many cases, the interest portion alone is sufficient to satisfy contingency fees, meaning the principal refund returns to your balance sheet as pure, unencumbered capital. This makes the decision to pursue a claim a low-risk, high-reward financial strategy for any CFO. You can begin this process immediately by requesting a preliminary Tariff Eligibility Assessment to see how much interest has already accrued on your entries. Treating this as a high-priority financial audit ensures you aren't leaving double-digit returns on the table.

Securing Your Full Recovery with Professional Auditing

Accepting a refund check from U.S. Customs and Border Protection (CBP) without a secondary audit is a risk your finance department shouldn't take. While the government maintains that their systems handle disbursements automatically, the reality of federal bureaucracy is far more prone to error. With approximately $100.65 billion in remaining IEEPA refund obligations still owed to importers as of June 2026, the sheer volume of these transactions creates significant room for systemic underpayment. The government’s priority is clearing the backlog; your priority is ensuring every cent of interest is accounted for.

Professional auditing serves as a necessary firewall between your balance sheet and automated government errors. When you understand how interest is calculated on tariff refunds, you realize that even a minor discrepancy in an entry date or a misapplied quarterly rate can result in a massive loss across a large portfolio. Relying on the government to self-correct these errors is not a viable financial strategy. Instead, you need a partner who views your recovery through the lens of assertive business advocacy, ensuring that the "all-in" value of your claim is fully realized.

The Importance of an Independent Audit

Automated government disbursements often fail to capture the nuances of complex trade entries. One frequent point of failure is the "liquidation" date. If CBP uses an incorrect date in their calculation engine, it can prematurely stop the interest clock, shaving weeks or months off your payout. These "minor" technicalities scale quickly. By reviewing How It Works, you'll see that our audit process involves a line-by-line verification of every entry. We compare the government's internal math against the statutory requirements of 19 U.S.C. § 1505 to identify and reclaim leaked capital.

Low-Risk Partnership for High-Stakes Recovery

Our contingency-fee model is designed to remove the financial risk of pursuing these complex claims. We only win when you recover your capital, which ensures our team is motivated to find every dollar. We manage the high-level legal gravitas and technical documentation required to challenge a refund amount, allowing your team to stay focused on core operations. We have the specialized tools to audit exactly how interest is calculated on tariff refunds for both corporate and non-corporate entities, protecting your right to the full 5% or 6% returns mandated for the 2026 fiscal year. Don't leave your interest on the table; get a preliminary Tariff Refund Assessment to see what you're truly owed.

Reclaim Your Capital with Total Precision

The window to recover billions in unlawfully collected IEEPA tariffs is open; however, the complexity of federal interest math remains a barrier for many firms. You've seen that interest isn't a bonus; it's a statutory right under 19 U.S.C. § 1505 designed to compensate you for the time your working capital was held by the Treasury. Because daily compounding and shifting quarterly rates can increase your total payout by 20% or more, an internal estimate is rarely enough. Understanding how interest is calculated on tariff refunds allows you to challenge government discrepancies and secure the full "all-in" recovery your business deserves.

We provide the specialized expertise and end-to-end documentation management required to navigate these high-stakes calculations. Our contingency-based model means there are no upfront costs; we only win when you successfully recover your capital. Don't leave your hard-earned interest in the government's accounts. Start your free IEEPA eligibility assessment and interest audit today. You've already done the hard work of paying these duties; now let us handle the heavy lifting of bringing that capital back to your balance sheet.

Frequently Asked Questions

Is interest on tariff refunds taxable as income?

Yes, the interest portion of your tariff refund is considered taxable income by the IRS and must be reported in the fiscal year it's received. While the principal refund of the duties you originally paid is typically not taxable because it's a return of capital, the interest is a separate financial gain. You should consult with your tax professional to ensure this recovery is categorized correctly on your balance sheet to avoid future compliance issues.

What is the current interest rate for duty refunds in 2026?

For the second quarter of 2026, which runs from April 1 through June 30, the interest rate for corporate overpayments is 5% per annum. Non-corporate entities receive a slightly higher rate of 6% for the same period. These rates are adjusted every three months by the IRS based on the federal short-term rate. Understanding how interest is calculated on tariff refunds during these specific windows is essential for projecting your total capital recovery from IEEPA claims.

Does the interest on tariff refunds compound daily or annually?

Interest on tariff overpayments compounds daily rather than annually. This requirement is mandated by 26 U.S.C. § 6622, ensuring that the value of your refund grows every 24 hours the government holds your funds. Daily compounding creates a significant "snowball effect" over the multi-year timelines common in IEEPA and Section 301 litigation. This mathematical nuance often adds thousands of dollars in value that a simple interest calculation would miss.

How long does it take to receive the interest after a refund is approved?

The interest is typically issued simultaneously with your principal refund check or electronic transfer. Once U.S. Customs and Border Protection approves the refund and the entry liquidates, the Treasury Department processes the payment. While the automation of the CAPE system has streamlined some of this, smaller firms or those with banking documentation issues may still experience delays. We monitor the federal payment cycle to ensure your funds arrive as quickly as possible.

Can I claim interest on Section 301 'China' tariffs?

Yes, you can absolutely claim interest on Section 301 "China" tariffs if those duties are found to be overpaid or are invalidated through legal action. The statutory right to interest under 19 U.S.C. § 1505 applies to all duty overpayments, not just those related to IEEPA. If your Section 301 entries are part of a successful protest or court ruling, the government must pay interest from the date you deposited the duties.

What happens if the government miscalculates my interest?

If the government miscalculates your interest, you have the legal right to challenge the disbursement through a formal protest. Many importers mistakenly assume that CBP's automated systems are infallible, but errors in liquidation dates or entity classification are common. An independent audit is the only way to verify the math. If a discrepancy is found, we handle the documentation required to force a correction and secure the remaining capital owed to you.

Do I need to file a separate request for the interest portion of my refund?

No, you don't need to file a separate request for the interest portion of your refund. Under federal law, interest is a statutory requirement that CBP must include automatically when a refund is issued. However, the government doesn't provide a detailed breakdown of their math. This lack of transparency is why many businesses choose to have their refunds audited to ensure the interest portion was calculated to the maximum legal limit.

Is the interest rate the same for all types of tariffs (IEEPA vs. Section 232)?

Yes, the interest rate is generally the same regardless of whether the refund stems from IEEPA, Section 301, or Section 232 duties. All trade-related overpayments follow the quarterly rates established by the Internal Revenue Code. The primary variables that change the payout aren't the tariff type, but your entity's corporate status and the specific dates the duties were held. This consistency allows for predictable modeling of your total recovery across different duty categories.

Ready to find out what your business may be owed?

Check My Eligibility