Over $175 billion in retail capital is currently sitting in government accounts instead of on your balance sheet due to an unconstitutional overreach of executive power. If your business paid duties under the International Emergency Economic Powers Act (IEEPA) since February 2025, you are likely sitting on a massive, untapped recovery opportunity. Securing a tariff refund for retailers is no longer a theoretical legal battle; it's a live financial restoration process with a strict 2026 deadline. You've likely felt the strain of these illegal duties on your cash flow while struggling to separate the IEEPA ruling from ongoing Section 301 trade disputes.

We understand the frustration of navigating the complex CAPE portal and the fear that bureaucratic delays might stall your recovery. This article provides a clear roadmap to help you reclaim your overpaid duties without the typical filing risks. You'll discover exactly how to manage your customs documentation for Phase 1 eligibility and learn the specific steps required to see your capital returned within the 60 to 90 day processing window established by U.S. Customs and Border Protection.

Key Takeaways

- Understand how the landmark Supreme Court ruling has unlocked a $166 billion recovery pool for importers who paid unconstitutional IEEPA duties.

- Distinguish your eligible IEEPA claims from ongoing Section 301 trade disputes to secure a successful tariff refund for retailers without legal confusion.

- Identify the specific documentation, including CBP Form 7501 and commercial invoices, required to successfully file through the new CAPE portal.

- Evaluate your standing as the Importer of Record to mitigate "double recovery" risks and navigate the complexities of the federal refund process.

- Learn how to leverage a contingency-based recovery model to reclaim capital before the three-year statute of limitations permanently closes the filing window.

The $160 Billion Retail Windfall: Why 2026 is the Year of Tariff Recovery

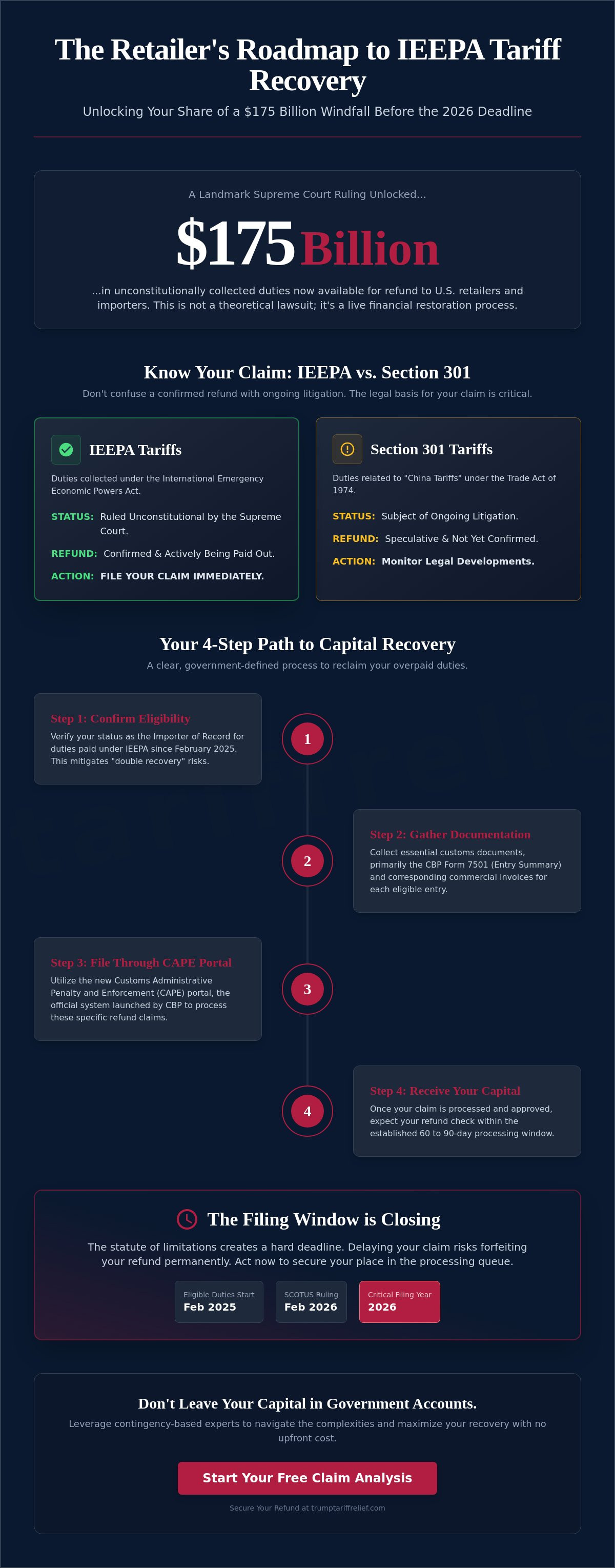

The American retail sector is currently witnessing the largest financial restoration in trade history. On February 20, 2026, the Supreme Court issued a landmark ruling that invalidated billions of dollars in tariffs. This decision confirmed that the executive branch overstepped its authority, creating a massive opening for businesses to recover capital that was taken unlawfully. We are not talking about small sums; the total pool of refundable duties is estimated between $164.7 billion and $175 billion. This isn't just a legal victory; it's a high-stakes opportunity to right a financial wrong.

For most businesses, this represents a chance to reclaim millions in overpaid duties. The primary beneficiaries are the Importers of Record, who paid these fees across more than 53 million separate entries. Because the government has already initiated the Phase 1 payout of $35.5 billion, the conversation has moved beyond legal debate. It's now a race against time to secure a tariff refund for retailers before the administrative windows begin to close. The government is no longer debating whether to pay; they're now focused on how quickly they can process these claims through new electronic systems.

The Legal Catalyst: SCOTUS and the IEEPA Overstep

The International Emergency Economic Powers Act (IEEPA) is a federal law that grants the President the power to regulate international commerce during a declared national emergency. The Supreme Court ruled that the recent expansion of these tariffs was an unconstitutional use of that power. The Court made it clear that emergency authority cannot be used as a permanent tool for standard trade policy. This ruling is the specific mechanism that allows your business to demand its money back. You can learn more about how this specific law applies to your imports by reading our IEEPA explained resource.

Economic Impact on the Retail Sector

Between 2018 and 2024, these tariffs acted as a massive tax on retail margins, forcing companies to choose between raising prices or absorbing losses. Reclaiming these funds is more than a refund; it's a strategic re-capitalization that can fund new growth or stabilize balance sheets. 2026 is the critical year for this recovery because U.S. Customs and Border Protection launched the CAPE portal on April 20, 2026, to centralize these claims. If you don't file your tariff refund for retailers now, you risk being pushed into later, more complex phases of the recovery program. The government started issuing the first checks on May 11, 2026, proving that the system is functional and ready for your claim. Delay only benefits the government's bottom line, not yours.

IEEPA vs. Section 301: Decoding the Legal Basis for Retailer Refunds

Distinguishing between different trade authorities is the first step toward a successful tariff refund for retailers. Many business owners mistakenly group all "China Tariffs" into a single category, but the legal reality is far more nuanced. While Section 301 duties remain a subject of ongoing litigation, the Supreme Court has already issued its final word on tariffs imposed under the International Emergency Economic Powers Act (IEEPA). This distinction is the difference between a pending "maybe" and a confirmed "now." Understanding the legal foundations of IEEPA is essential for any importer looking to separate confirmed recovery opportunities from speculative court cases.

The Court of International Trade played a pivotal role in validating these refunds by highlighting the specific instances where executive authority overstepped its bounds. When the government uses emergency powers to bypass traditional legislative trade routes, it creates a window for legal restoration. The current refund program specifically targets duties collected from February 4, 2025, onward, providing a clear path for retailers to reclaim capital that was never legally authorized. This process is governed by the CBP Trade Remedies framework, which now includes the CAPE portal to facilitate these specific claims.

Section 301 List 3 and List 4A Explained

The vast majority of retail goods, including electronics, apparel, furniture, and home goods, were hit hardest by "List 3" and "List 4A" designations. These lists covered billions in annual imports, significantly compressing retail margins for years. It is vital to identify which of your entries were paid under IEEPA authority versus standard Section 301 duties. While List 3 and 4A goods are often the focus of trade disputes, only those entries specifically tied to the unconstitutional IEEPA expansion are currently eligible for the 60 to 90 day refund window. Identifying these specific entries is the first step in our comprehensive eligibility assessment.

Why General Customs Brokers May Miss the Nuance

Standard customs brokers are excellent at managing "duty drawbacks," which involve reclaiming tariffs on goods that are subsequently exported. However, a tariff refund for retailers based on an unconstitutional ruling requires a different level of expertise. This is not a routine administrative filing; it is an unlawful tariff recovery that demands a specialized audit of your import history. General brokers often lack the technical legal infrastructure to navigate the CAPE portal's specific requirements for IEEPA claims. Because this recovery is based on a Supreme Court ruling rather than a standard trade policy change, a dedicated recovery audit is the only way to ensure no capital is left behind.

Eligibility and the 'Double Recovery' Risk: Can Your Retail Business Claim?

Determining your eligibility for a tariff refund for retailers begins with a single question: were you the Importer of Record (IOR) for the entries in question? While approximately 330,000 importers are affected by the IEEPA ruling, the government only recognizes the entity that legally paid the duties to CBP. If your business is the one listed on the Entry Summary, the right to recovery is yours. This is a high-stakes financial restoration, and confirming your status is the first step toward reclaiming your share of the $166 billion pool. If you're unsure about your specific entry types or dates, you should check our FAQ for eligibility questions to clarify your standing.

The Importer of Record Requirement

The legal right to file a claim rests exclusively with the entity that fulfilled the payment obligation to U.S. Customs and Border Protection. If your retail business has undergone a merger or acquisition since the duties were paid, the successor entity typically inherits the right to the refund. However, this requires meticulous documentation to prove the transfer of assets and legal claims. You must have a valid Employer Identification Number (EIN) and an active CBP account to facilitate the filing. Without these verified credentials, your claim will not move through the automated CAPE portal, regardless of how much you overpaid.

Navigating the PR and Legal Trap

A significant point of contention has emerged regarding the "double recovery" controversy, often highlighted by outlets like Forbes. Critics argue that retailers shouldn't keep refunds if they already passed the tariff costs on to consumers through higher shelf prices. Legally, the fact that you passed costs to consumers does not waive your right to a refund of unconstitutionally collected duties. The Supreme Court's ruling focused on the government's overreach, not your internal pricing strategies. The capital belongs to the business from which it was unlawfully taken.

As noted by the National Retail Federation on IEEPA tariff refunds, the industry is already seeing downstream litigation. Class-action lawsuits have been filed against major retailers by customers demanding a share of the windfall. To mitigate this risk, successful businesses are proactively framing their tariff refund for retailers as a tool for re-capitalization. Re-investing this capital into price cuts, infrastructure, or domestic expansion creates a powerful narrative of corporate responsibility. It's about reclaiming what is legally yours while strategically positioning those funds to drive future growth and consumer value.

The CAPE Portal and Beyond: Essential Documentation for Retail Claims

The launch of the Consolidated Administration and Processing of Entries (CAPE) portal on April 20, 2026, transformed the recovery landscape for U.S. importers. This digital gateway is now the official system for reclaiming capital unconstitutionally collected under IEEPA authority. To successfully secure a tariff refund for retailers, your business must transition from fragmented paper trails to a structured electronic format within the ACE Portal. CBP anticipates processing valid claims within 60 to 90 days, but this aggressive timeline depends entirely on the precision of your digital records. If your data is incomplete, your claim will likely be sidelined during the initial Phase 1 payout period.

Successful recovery requires a high level of administrative discipline. You must be prepared to submit a "consolidated declaration" that groups your eligible entries into a single, verifiable package. This is a departure from traditional, entry-by-entry protests. The government is moving quickly to clear the backlog, but they are using automated filters to flag discrepancies. You can see our step-by-step process guide to understand how to prepare your data for this new electronic environment.

The CAPE Portal Workflow

The CAPE workflow is designed to handle the massive volume of 53 million separate import entries. Phase 1 of the program is specifically limited to unliquidated entries and those liquidated within 80 days of the claim submission. If your entries fall outside this narrow window, they will be addressed in later, more complex phases. The most common reasons for rejection in this new system include mismatched Importer of Record (IOR) numbers and incorrect entry types. The system is built for efficiency, but it will automatically kick out any declaration that does not align with CBP’s internal database.

Audit-Proofing Your Retail Claim

The core of your claim rests on two critical documents: the Entry Summary (CBP Form 7501) and your commercial invoices. You must verify that the Harmonized Tariff Schedule (HTS) codes used at the time of entry match the specific categories invalidated by the Supreme Court. It's not enough to show that duties were assessed; you must prove they were actually paid. Secondary verification by a third party is the best defense against government pushback. Mismatched HTS codes or missing payment confirmation are the primary triggers for a manual audit, which can delay your refund by months. Ensure your claim is bulletproof by starting our customs documentation management assessment today.

Maximizing Your Recovery: Why Retailers Choose Contingency-Based Experts

Reclaiming unconstitutionally collected duties is not a routine administrative task; it is a high-stakes financial recovery operation. While the CAPE portal provides the infrastructure for a tariff refund for retailers, navigating that system requires a level of specialization that standard customs brokers rarely possess. Most businesses are faced with a choice: attempt to manage a multi-year recovery project internally or partner with experts who operate on a success-based model. A contingency-fee structure eliminates upfront risk, ensuring that your interests and your partner's goals are perfectly aligned. You don't pay for the effort of filing; you only pay when the capital is back on your balance sheet.

There is a significant difference between simply "filing a claim" and actually "winning a recovery." The government’s automated filters in the CAPE system are designed to identify any reason for a denial. Without a dedicated team to manage the heavy lifting of data validation and legal positioning, retailers often find their claims stalled in the "review" phase indefinitely. By leveraging specialized expertise, you ensure that your documentation is not just submitted, but optimized to pass through CBP’s multi-phase review without friction.

The 3-Year Deadline: A Fleeting Window

The statute of limitations for IEEPA claims creates a hard wall that many retailers overlook. Under current trade laws, you generally have a three-year window from the date of entry liquidation to secure your right to a refund. Waiting for "perfect clarity" from the government is a dangerous strategy that often results in missed deadlines. Trade lawyers have already flagged the possibility of last-minute administrative appeals that could further complicate the filing process for latecomers. If you don't act while the Phase 1 and Phase 2 windows are open, you risk forfeiting your share of the $175 billion pool permanently.

The Power of a Contingency Partner

Internal logistics and finance teams are already overwhelmed by day-to-day operations and supply chain volatility. Managing a tariff refund for retailers involves auditing thousands of entries across years of trade history, a task that can take hundreds of man-hours. A contingency partner acts as an extension of your firm, taking on the technical burden without adding to your overhead. We provide the sophisticated navigation required to bypass bureaucratic delays, allowing your team to stay focused on growth while we recover your lost capital.

The window to reclaim your unconstitutional tariff payments is closing as the 2026 deadlines approach. Securing your firm’s financial future requires immediate, decisive action. Don't leave your capital in the government's hands when a risk-free path to restoration is available. Start your Tariff Eligibility Assessment today and ensure your retail business receives the full recovery it is legally owed.

Reclaim Your Capital Before the Window Closes

The path to financial restoration is now open, but it won't stay that way forever. By distinguishing your IEEPA-eligible entries from broader trade disputes and mastering the CAPE portal's documentation requirements, you can recover significant capital that was taken unlawfully. This process is about righting a financial wrong and re-capitalizing your business for future growth. Securing a tariff refund for retailers requires a specialized approach that goes beyond standard customs brokerage, focusing on the technical nuances of IEEPA litigation.

We provide the specialized expertise and end-to-end management needed to navigate this bureaucratic maze. Because we work on a contingency basis, you face zero upfront risk. If we don't recover your funds, you don't pay a fee. Our team handles the heavy lifting, from initial documentation audits to final filing, so you can stay focused on your operations. Don't let your capital remain in government accounts when it belongs on your balance sheet.

Take the first step toward reclaiming what is yours. Get Your Free Retail Tariff Eligibility Assessment and secure your firm's financial future today. Your successful recovery is our only priority.

Frequently Asked Questions

Is the China tariff refund for retailers real?

Yes, this is a confirmed financial restoration program following the Supreme Court’s February 20, 2026, ruling that invalidated specific IEEPA duties. U.S. Customs and Border Protection has already established the CAPE portal to process these claims. With an estimated $175 billion available for recovery, the government began issuing the first wave of payments to early filers in mid-May 2026.

What is the deadline to file for an IEEPA tariff refund in 2026?

The deadline is dictated by a three-year statute of limitations; however, the immediate window for Phase 1 is much tighter. Currently, the CAPE system prioritizes unliquidated entries and those liquidated within 80 days of your claim submission. Waiting for the final deadline risks missing the streamlined Phase 1 and Phase 2 payout cycles, which are designed for rapid processing.

How long does it take for a retailer to receive a tariff refund check?

CBP typically issues refunds within 60 to 90 days after they accept your CAPE Declaration. These payments are processed electronically via the ACE Portal and include interest as required by 19 U.S.C. § 1505. Because the system is now automated, retailers with clean documentation are seeing significantly faster turnaround times than traditional manual protest filings.

Can I claim a refund if I already passed the tariff costs to my customers?

Yes, your right to recovery is independent of your retail pricing strategy. As the Importer of Record, you are the entity that legally paid the unconstitutional duties to the government. The legal basis for a tariff refund for retailers rests on the fact that the capital was taken unlawfully from your business, regardless of how you managed your downstream margins.

What is the difference between Section 301 and IEEPA refunds?

IEEPA refunds are confirmed and active, while Section 301 refunds remain speculative and tied to ongoing litigation. The February 2026 ruling specifically targeted the misuse of emergency powers under the International Emergency Economic Powers Act. While many retail goods are subject to both, only the duties paid under the invalidated IEEPA authority are currently eligible for immediate 60 to 90 day payouts.

Do I need a customs broker or a specialized consultant for this claim?

Most standard customs brokers lack the technical legal infrastructure to navigate the new CAPE portal's litigation-based requirements. While brokers handle routine entries, a tariff refund for retailers requires a specialized audit to separate eligible IEEPA entries from standard duties. Specialized consultants provide the end-to-end management and data validation necessary to ensure your claim isn't rejected by CBP's automated filters.

What happens if the government appeals the IEEPA ruling?

The Supreme Court’s decision is the final authority, meaning the unconstitutionality of these specific duties is settled law. While the administration may attempt to introduce new trade investigations under different authorities, they cannot retroactively undo the ruling that made these past payments illegal. The right to reclaim this capital is secured for any importer who meets the filing requirements.

Which retail products are eligible for the List 3 and List 4A refunds?

Eligibility is determined by the legal authority used to collect the duty, not just the product category. However, most apparel, electronics, and home goods imported under List 3 and List 4A from February 4, 2025, onward are likely candidates for recovery. We recommend a full eligibility assessment to verify that your specific HTS codes were assessed under the invalidated IEEPA emergency declarations.

Ready to find out what your business may be owed?

Check My Eligibility