Every day your corporate capital remains locked in a government account is a day it isn't fueling your growth. The strict 180-day deadline to challenge a liquidated entry acts as a silent trap, often foreclosing refund rights before a business even realizes a mistake was made. If you're currently disputing Section 301 tariffs, you're likely facing the added pressure of the June 2026 announcements regarding new investigations into Vietnam and Brazil. It's frustrating to watch your margins erode while trade policies shift, but these overpaid duties don't have to be a permanent loss for your bottom line.

We recognize the confusion many importers feel when trying to distinguish between Section 301 and IEEPA recovery paths. This guide promises to clarify that complexity by providing the exact legal grounds and administrative steps required to file a formal protest and recover your payments. You'll learn the mechanics of successfully filing CBP Form 19, how to preserve your right to sue in the Court of International Trade, and the specific process for securing a full recovery of your duties on a contingency basis.

Key Takeaways

- Understand how 19 U.S.C. § 1514 serves as the definitive statutory mechanism for reclaiming overpaid duties in the 2026 trade environment.

- Identify why the 180-day deadline begins at the moment of liquidation to ensure your business doesn't forfeit its right to a refund.

- Learn the specific legal arguments for disputing Section 301 tariffs, focusing on exceeded statutory authority and product misclassification.

- Master the administrative requirements of CBP Form 19, including the critical narrative components required for a successful Statement of Grounds.

- Leverage a contingency-based recovery model to reclaim locked corporate capital without the burden of upfront legal fees.

The Legal Basis for Disputing Section 301 Tariffs: 19 U.S.C. § 1514

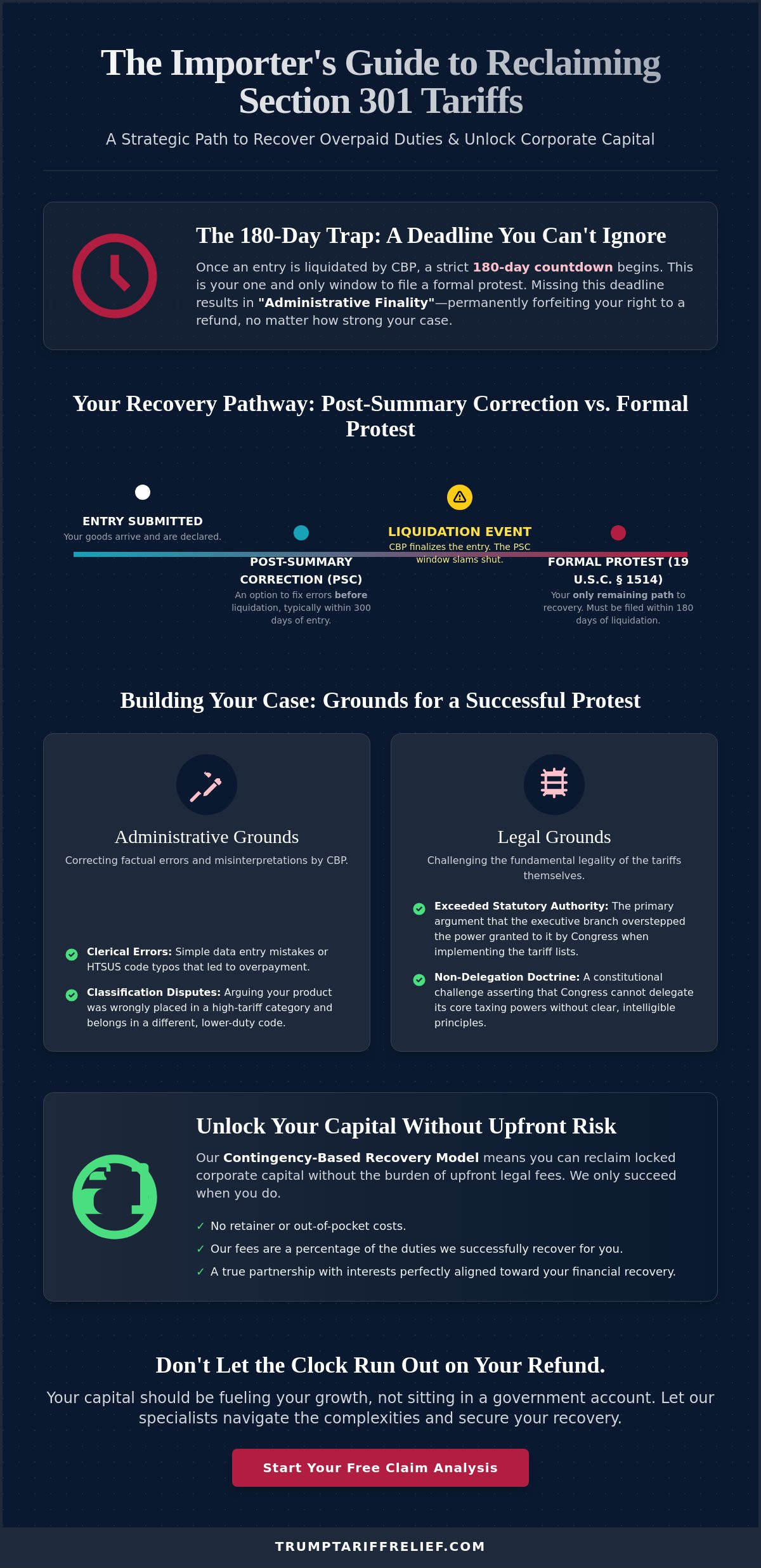

When you're disputing Section 301 tariffs, you aren't just filing a complaint; you're exercising a statutory right under 19 U.S.C. § 1514. This specific section of the law is the primary legal mechanism for challenging decisions made by U.S. Customs and Border Protection (CBP). Without it, the government's determination on your duties would be final and unchangeable. The statute allows importers to contest a wide range of CBP actions, including the classification of goods, the valuation of merchandise, and, most importantly, the imposition of additional duties under Section 301 of the Trade Act of 1974.

It's vital to distinguish between a Post Summary Correction (PSC) and a formal Protest. A PSC is a correction submitted before an entry liquidates, typically within 300 days of entry. However, once CBP liquidates the entry, the PSC window slams shut. At that point, a formal Protest under Section 1514 becomes your only shield. You have exactly 180 days from the date of liquidation to file. If you miss this hard deadline, you face "administrative finality," a legal state where your right to recover overpaid duties is permanently foreclosed, regardless of how strong your legal argument might be.

Administrative vs. Legal Grounds for Recovery

Disputes generally fall into two categories: administrative errors and legal challenges. Administrative grounds often involve clerical mistakes or HTSUS misclassifications where a product was wrongly placed in a high-tariff category. Legal grounds are more significant. These challenges argue that the executive branch exceeded its delegated authority from Congress when it implemented or expanded the tariff lists. While administrative fixes are routine, legal grounds offer a path to disputing Section 301 tariffs on a systemic level, potentially reclaiming millions in locked corporate capital that was collected under questionable statutory authority.

- Clerical Errors: Simple data entry mistakes or HTSUS code typos.

- Classification Disputes: Arguing your product belongs under a different, duty-free code.

- Statutory Authority: Challenging whether the tariffs were legally enacted under the Trade Act.

The Intersection of IEEPA and Section 301

The International Emergency Economic Powers Act (IEEPA) has become a central pillar in modern trade disputes. While Section 301 focuses on "unfair trade practices," the government often uses IEEPA authority to justify rapid, sweeping tariff increases during national emergencies. Current legal strategies often target the "reciprocal" nature of these duties, arguing that the administration has used these powers to bypass the specific limitations set by Congress. Understanding this overlap is essential for any business looking to secure a refund. You can find a deeper dive into these specific legal nuances in our guide on IEEPA Explained, which details how these two authorities interact to impact your bottom line.

Primary Grounds for Filing: Challenging Statutory Authority

Successful filing requires more than just a vague objection; it demands a precise narrative that identifies exactly where the government overstepped its bounds. When disputing Section 301 tariffs, the most potent argument often involves the "Exceeded Authority" claim. This strategy challenges whether the executive branch actually possessed the delegated power from Congress to impose specific duties on certain categories of goods. As highlighted by Brookings on Section 301 investigations, the evolving nature of these trade actions creates a fluid legal landscape where legal challenges can expose cracks in executive enforcement.

Beyond statutory limits, the non-delegation doctrine provides a constitutional ground for recovery. This argument asserts that Congress cannot hand over its taxing power to the executive branch without clear, intelligible principles. If an Executive Order lacks this clarity, or if CBP enforcement deviates from the original order's intent, the duty imposition may be legally void. Identifying these discrepancies requires a granular review of Federal Register notices against your specific entry data. We often find that CBP's actual enforcement on the ground doesn't always align with the narrow scope of the President's initial directives.

Exceeding the Scope of National Emergency Authority

The International Emergency Economic Powers Act (IEEPA) was designed for defensive measures during true national crises, not as a general revenue tool for the Treasury. Importers can argue that reciprocal trade actions, which mirror another country's tariffs, don't meet the "emergency" threshold required by law. By 2026, a legal consensus has emerged that executive trade reach must be tethered to specific, documented threats. If your duties were applied under a broad emergency declaration that doesn't directly relate to your industry, you have strong grounds for a protest. IEEPA wasn't intended to give the executive branch a blank check for trade wars.

Improper Application of Reciprocal Duty Rates

Many businesses discover their products were miscategorized into a high-tariff list due to over-broad HTSUS code applications. You must argue that your specific goods don't fall within the scope of the Federal Register notices that authorized the tariffs. Using historical entry data is critical here to prove that CBP has applied these codes inconsistently in the past. If you're unsure if your products were miscategorized, a professional Tariff Eligibility Assessment can help identify these high-value recovery opportunities. Proving that your goods were swept into a list where they don't belong is a primary path to reclaiming your capital.

Eligibility and Standing: Who Can File and When?

Standing isn't a formality. It's the legal foundation of your entire recovery strategy. Only the entity listed as the Importer of Record (IOR) possesses the legal standing to challenge CBP decisions under 19 U.S.C. § 1514. In complex, multi-national supply chains, identifying the correct IOR can be surprisingly difficult, especially when third-party logistics providers or various subsidiaries are involved. If you file a protest under the wrong entity name, CBP will dismiss it immediately, and you'll likely be past the deadline to fix the error. You must ensure the party disputing Section 301 tariffs is the same party that paid the duties and holds the legal liability for the entry.

Timing is the most common reason refund claims fail. The law provides a strict 180-day window to file a protest, but the clock doesn't start when your goods arrive at the port. It starts at "Liquidation," the moment CBP officially finalizes the entry. If you miss this hard deadline by even 24 hours, your right to a refund is permanently foreclosed. There's no "good faith" exception for missing this window; once the 180 days expire, the government's decision becomes administratively final and unchallengeable.

The 180-Day Liquidation Window

Liquidation is the final step in the customs process where CBP calculates the exact duties owed and closes the file on an entry. While this usually happens within 314 days of entry, CBP can extend this period for years. You must track your liquidation dates through the ACE (Automated Commercial Environment) portal to avoid being blindsided. Strategic timing is critical here. If you file a protest before the entry actually liquidates, CBP might reject it as premature. You need to hit the sweet spot: after liquidation occurs, but before the 180-day clock runs out. If you're struggling to track these dates, our FAQ provides more details on monitoring your entry status.

Protective Protests for Ongoing Litigation

A protective protest is a specialized legal tool used to stop the clock while major court cases are decided. For example, many importers are currently disputing Section 301 tariffs by referencing the IEEPA Supreme Court challenge or other lead cases in the Court of International Trade. By filing a protective protest, you preserve your right to a refund even if the court takes years to reach a final verdict. High-volume national importers should maintain a rigorous "protest log" to ensure every eligible entry is captured. This systematic approach prevents your capital from being trapped by bureaucratic delays or shifting legal precedents. You can learn more about how we manage these complex filings in our recovery process overview.

The Step-by-Step Filing Process for CBP Form 19

Filing a protest isn't a mere administrative task; it's a high-stakes legal maneuver that requires absolute precision. When you're disputing Section 301 tariffs, your success depends entirely on the technical accuracy of your documentation. The process begins with a comprehensive audit of your records to gather every Entry Summary (CBP Form 7501) associated with the impacted shipments. These forms contain the specific entry numbers, liquidation dates, and HTSUS codes that serve as the bedrock of your claim. Once your data is organized, you'll submit the protest through the Automated Commercial Environment (ACE) portal. This electronic module is the only reliable way to ensure your filing is officially recorded and to secure a Protest Number for real-time tracking.

After submission, you must remain vigilant. CBP often responds with a Form 28, which is a formal Request for Information. This isn't a casual inquiry; it's a test of your claim's validity. You must provide detailed product specifications and HTSUS justifications that align perfectly with your original protest. If your response is weak or inconsistent, CBP will use it as grounds for an immediate denial, effectively locking your capital away for good.

Drafting a Bulletproof Statement of Grounds

Generic complaints are the fastest route to a rejection. CBP officials aren't authorized to build your case for you; they're looking for reasons to uphold the original duty assessment. Your "Statement of Grounds" must be a rigorous legal narrative that cites specific statutory violations and references the 2026 IEEPA ruling specifically. For example, a successful filing might include a sentence like this: "The imposition of duties on HTSUS 8501.10.4020 under the current executive directive exceeds the reciprocal authority granted by Congress, as established in the 2026 IEEPA appellate findings." This level of legal specificity forces the government to address the merits of your dispute rather than dismissing it as a clerical error.

Managing High-Volume Filings

For national importers with thousands of shipments, filing individual protests is a logistical nightmare. The most effective strategy is grouping entries by their specific legal grounds to streamline the review process and ensure consistency across your entire portfolio. While traditional customs brokers are excellent at moving freight, they often lack the specialized legal bandwidth required for high-stakes disputing Section 301 tariffs. Specialized recovery consultants fill this gap by providing the narrative expertise needed to win. You can learn more about how we optimize this complex cycle by reviewing our How It Works page. If you're ready to reclaim your overpaid duties without the risk of upfront costs, start your Tariff Eligibility Assessment today to see which entries are ripe for recovery.

Strategic Recovery: Why Professional Filing Protects Your Capital

Attempting to handle these complex filings internally often results in the permanent foreclosure of your refund rights. When disputing Section 301 tariffs, a single technical error in your Statement of Grounds can lead to a summary denial from CBP. Once denied, the window to correct the narrative or resubmit the claim typically vanishes. Professional filing isn't just about administrative convenience; it's a strategic safeguard for your corporate capital. Specialized trade experts bring a level of forensic detail that in-house teams frequently overlook, identifying secondary grounds such as valuation discrepancies or obscure HTSUS exclusions that can significantly increase the total recovery amount.

Busy executives don't have the bandwidth to monitor liquidation cycles or draft 20-page legal briefs. Our "we-do-the-work" partnership model ensures that the heavy lifting remains with the experts while your team remains focused on core operations. We act as the active engine of recovery, managing the entire lifecycle from the initial entry audit to the final disbursement of funds. This approach transforms a complex bureaucratic hurdle into a streamlined financial win for your organization.

Contingency Models: Aligning Incentives

The traditional legal model, built on expensive hourly retainers, often creates a financial barrier to justice. If the cost of the legal work approaches the value of the potential refund, the ROI disappears. A contingency-based recovery model eliminates this risk entirely. By operating on a percentage-of-recovery basis, our incentives are perfectly aligned with yours; we only win when you win. This "Zero Upfront Cost" promise is particularly critical for 2026 corporate budgets, allowing firms to pursue high-value claims without adding to their fixed overhead. Compared to internal attempts that drain staff time and resources, professional recovery offers a streamlined, low-risk path to financial restoration.

Next Steps: Your Preliminary Assessment

The clock is ticking on your 2026 statutory deadlines. Every day an entry remains liquidated without a protest is a day closer to losing those funds forever. To begin the recovery process, we recommend a professional audit of your past tariff payments to identify which entries meet the criteria for a successful challenge. This preliminary assessment is the first step toward reclaiming your locked capital. Don't let administrative inertia stand in the way of your company's rightful funds. Get your free IEEPA eligibility assessment today and secure the professional guidance needed to navigate the complexities of disputing Section 301 tariffs.

Reclaim Your Capital and Restore Your Margins

The window for action is narrow, and the stakes for your corporate capital couldn't be higher. Successfully disputing Section 301 tariffs requires a deep understanding of the 180-day liquidation window and the precise statutory grounds under 19 U.S.C. § 1514. Relying on generic administrative corrections is often a recipe for a permanent denial. You need a strategy that leverages the latest 2026 legal precedents and identifies every HTSUS misclassification or executive overreach that has impacted your bottom line.

Our specialized IEEPA legal and trade experts take the entire burden off your shoulders, providing complete documentation management from the initial filing to the final refund. Because we operate on a contingency basis, you only pay if we recover your money. This is a low-risk opportunity to right a financial wrong and reclaim what belongs to your business. Your overpaid duties represent locked potential; it's time to bring that capital back home. Secure Your IEEPA Refund Assessment and let us start the work of restoring your financial strength today.

Frequently Asked Questions

What are the most common grounds for a tariff protest denial?

The most common grounds for a protest denial are missing the strict 180-day filing window after liquidation or failing to establish legal standing as the Importer of Record. CBP also frequently rejects claims that provide vague or generic objections without citing specific statutory violations. When disputing Section 301 tariffs, your narrative must be technically precise and legally grounded to survive a secondary review by Customs officials.

Can I file a protest if my entry has not yet liquidated?

You cannot file a formal protest until your entry has officially liquidated. Filing before this date is considered premature and will lead to an immediate administrative rejection. If you need to correct an entry before liquidation occurs, you should utilize a Post Summary Correction (PSC). Once the liquidation status is finalized in the ACE portal, the 180-day clock begins, and the protest mechanism becomes your primary legal remedy.

How long does CBP have to decide on a tariff protest?

CBP typically has two years to decide on a protest, though many decisions are reached much faster depending on the complexity of the legal grounds. If your business requires a rapid resolution, you can file a request for "accelerated disposition." This forces CBP to issue a decision within 30 days of the request. If they fail to act within that timeframe, the protest is deemed denied, allowing you to move the case to court.

What is the difference between a Section 301 protest and an IEEPA protest?

A Section 301 protest typically challenges the classification or inclusion of a product on a specific tariff list, whereas an IEEPA protest challenges the President's underlying authority to impose those duties. While both mechanisms are used when disputing Section 301 tariffs, the IEEPA path often targets the broader constitutional and statutory limits of executive trade power. Combining these arguments provides a more robust defense of your corporate capital.

Do I need a lawyer to file a CBP Form 19 protest?

You don't legally need a lawyer to file CBP Form 19, but attempting a DIY filing is extremely risky for complex trade disputes. The "Statement of Grounds" requires sophisticated legal citations and a deep understanding of trade statutes that go beyond standard brokerage capabilities. Professional recovery experts ensure that every technical requirement is met, protecting you from the administrative errors that lead to permanent foreclosure of your refund rights.

What happens if my protest is denied by Customs?

If Customs denies your protest, your next step is to file a summons and complaint in the U.S. Court of International Trade (CIT). You have exactly 180 days from the date of the protest denial to initiate this litigation. This transition from an administrative dispute to a judicial one is a critical phase that requires specialized legal expertise to preserve your right to a full recovery of overpaid duties.

Can I group multiple entries into a single protest filing?

You can group multiple entries into a single protest filing provided they involve the same legal issues and were liquidated at the same port. This strategy is highly efficient for high-volume importers who need to challenge hundreds of similar shipments simultaneously. Grouping entries helps streamline the CBP review process and ensures that your legal arguments remain consistent across your entire portfolio of impacted shipments.

Is there a fee to file a protest with CBP?

There is no government filing fee to submit an administrative protest with CBP. This makes the protest a low-cost first step in the recovery process. However, if the protest is denied and you choose to escalate the matter to the Court of International Trade, you'll be responsible for court filing fees and related legal costs. Our contingency model ensures that these initial administrative steps don't drain your corporate budget.

Ready to find out what your business may be owed?

Check My Eligibility