Your business has likely overpaid millions in duties to the U.S. Treasury, and the window to secure your Section 301 refund for automotive parts is rapidly closing as the April 2026 deadlines approach. Recent landmark rulings have finally exposed the extent of these overpayments, yet the complexity of the recovery process remains a significant barrier for even the most sophisticated importers. You've spent years absorbing the impact of aggressive trade policies and managing dense documentation, often while fearing that an aggressive claim might trigger a disruptive CBP audit. It's a high-stakes environment where the system often feels designed to keep your capital out of your hands.

We believe it's time to right that wrong. This guide provides the definitive, step-by-step framework to reclaim your overpaid IEEPA and Section 301 duties following the court decisions that have shifted the regulatory landscape in your favor. You'll learn how to utilize a managed filing process to recover your capital with zero upfront financial risk. We'll detail exactly how to identify eligible entries and meet the strict 2026 filing requirements, ensuring your recovery is handled with the professional gravitas and precision your bottom line deserves.

Key Takeaways

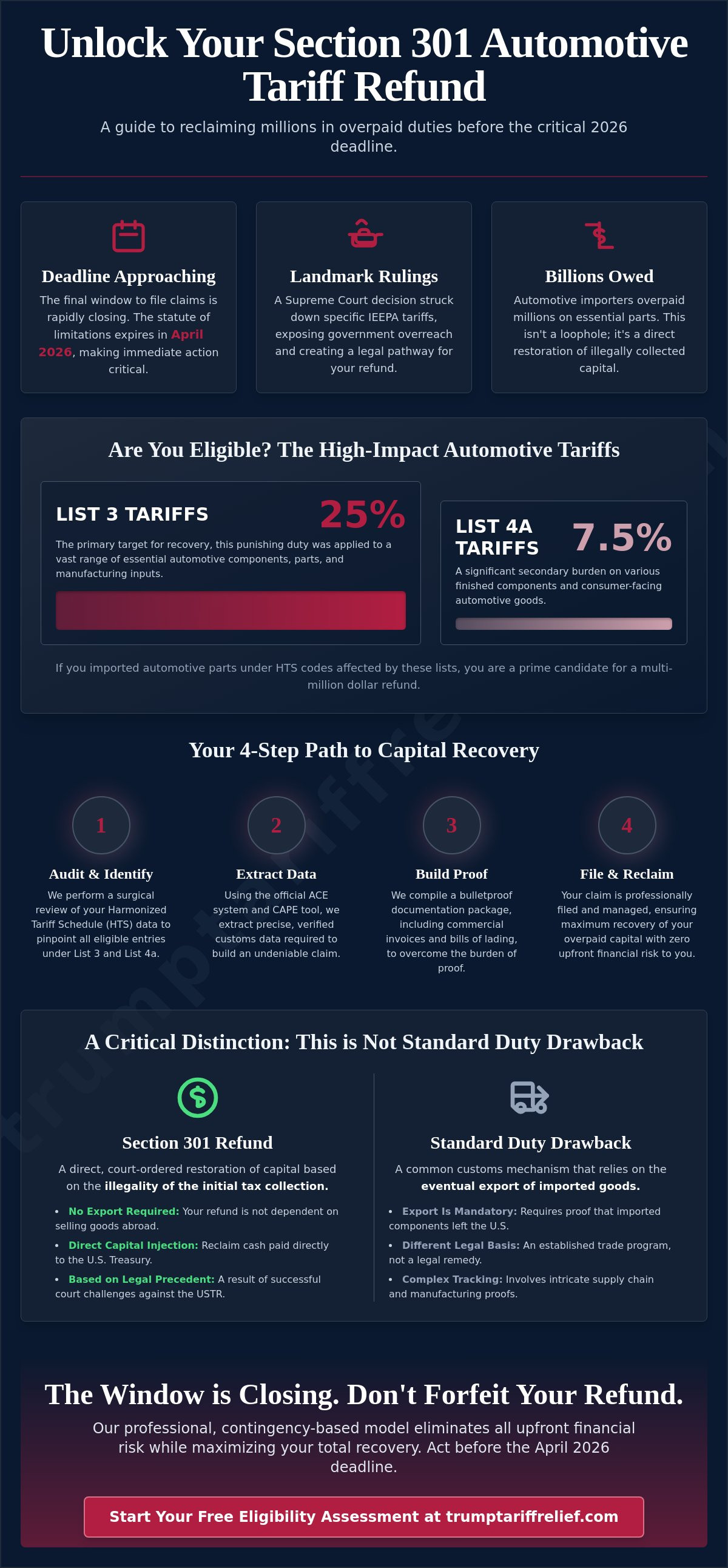

- Understand how the Supreme Court strike-down of IEEPA tariffs and the April 2026 deadlines create an immediate, high-stakes window for duty recovery.

- Identify which high-value HTS codes qualify for a Section 301 refund for automotive parts, specifically targeting the significant duties paid under List 3 and List 4a.

- Master the technical requirements for navigating the ACE system and the CAPE tool to ensure accurate data extraction for your claim.

- Build a bulletproof documentation strategy using commercial invoices and bills of lading to overcome the burden of proof and avoid claim rejections.

- Leverage a professional contingency-based model to manage the entire filing process, eliminating upfront financial risk while maximizing your total recovery.

The 2026 Landscape for Automotive Section 301 and IEEPA Refunds

A landmark Supreme Court ruling has fundamentally altered the trade landscape by striking down specific tariffs previously authorized under the International Emergency Economic Powers Act (IEEPA). This decision isn't just a legal victory; it's a financial catalyst for automotive importers who have spent years absorbing aggressive duties. By challenging the government's overreach, the courts have opened a pathway to reclaim billions in overpaid capital. If your company imported components under Section 301 List 3 or List 4a, you are likely eligible for a substantial Section 301 refund for automotive parts. This recovery opportunity exists because the judiciary found that the executive branch exceeded its statutory authority when it expanded tariffs beyond the original scope of the trade investigations.

Time is your greatest adversary in this process. The statute of limitations on entry liquidations means that once an entry is legally finalized by Customs and Border Protection (CBP), the opportunity to protest or reclaim those funds vanishes forever. The 2026 window represents the final opportunity to audit the years of peak tariff activity and secure a recovery before these entries are sealed. It's vital to distinguish this from standard duty drawbacks. While drawbacks rely on the eventual export of finished goods, the IEEPA refund opportunity is a direct restoration of capital based on the illegality of the initial collection. You don't need to export anything to qualify; you simply need to prove you paid a duty that should never have been levied.

Why Automotive Importers are Prime Candidates for Recovery

Automotive manufacturers and Tier 1 suppliers are the primary victims of List 3 duties, which imposed a 25% tax on a vast array of essential components. These tariffs were often justified by investigations into structural excess capacity, yet they effectively acted as a massive tax on domestic assembly lines. Reclaiming this capital now provides a critical buffer against the rising logistics and labor costs that continue to squeeze margins across the sector in 2026. Just as logistics managers might consult the Truck Accident Calculator to evaluate operational risks and claims, identifying overpaid duties allows firms to quantify and recover significant lost capital. Because the automotive supply chain is so reliant on high-volume List 3 entries, the potential for a multi-million dollar recovery is significantly higher than in other industries.

Understanding the IEEPA vs. Section 301 Overlap

The overlap between IEEPA and Section 301 of the Trade Act of 1974 created a scenario where many automotive parts were effectively double-taxed or trapped in incorrect HTS categories. The legal basis for the current recovery efforts rests on the fact that the USTR exceeded its authority when applying manufacturing overcapacity penalties through IEEPA rather than following the strict procedural requirements of Section 301. An IEEPA tariff refund is a court-ordered restoration of overpaid manufacturing duties. To understand the specific legal mechanisms at play, you can explore how IEEPA recovery works for your specific import history.

Identifying Eligible Automotive Parts and HTS Codes

Securing a Section 301 refund for automotive parts requires a surgical review of your Harmonized Tariff Schedule (HTS) data. Many importers simply absorbed these duties as an unavoidable cost of doing business, but the recent legal shifts demand a more aggressive posture. You must audit your import history to isolate entries tied to List 3 and List 4a. List 3, which carried a punishing 25% duty rate, encompassed the vast majority of mid-tier automotive manufacturing inputs. List 4a added a 7.5% burden on various finished components. Identifying these specific entries is the first step in reclaiming capital that was collected under a now-contested legal authority.

Verification hinges on whether your specific parts fall under the struck-down IEEPA authority. This isn't a general "catch-all" recovery. It's a targeted strike on duties that were expanded beyond the original Section 301 investigation's scope. If your parts were categorized under HTS codes that saw rate hikes during the 2018 to 2020 expansion windows, they are likely prime candidates for a full restoration of funds. You don't have to guess about your eligibility. A professional tariff eligibility assessment can quickly categorize your import history and quantify the total recovery available to your business.

High-Priority Automotive Categories for Claims

Certain sectors of the automotive supply chain were hit harder than others, making them high-value targets for recovery. Chassis components and suspension systems found in HTS Chapter 87 represent some of the largest potential claims due to their high unit value and consistent import volume. Electronic control units (ECUs) and semiconductor-heavy assemblies also qualify, particularly those that were caught in the crossfire of manufacturing overcapacity investigations. Additionally, electric vehicle (EV) battery components and thermal management systems represent a growing category of eligible entries that many importers overlook.

The "Substantial Transformation" Rule in Auto Parts

The complexity of modern supply chains often obscures the true origin of a part, leading to massive overpayments. If you imported components from third countries like Vietnam, Mexico, or Thailand that utilized China-sourced materials, you may have been incorrectly charged Section 301 duties. Misinterpretation of the "substantial transformation" rule by both importers and CBP led to duties being applied to goods that should have been exempt. Identifying "hidden" eligibility in these sub-assemblies and replacement parts can significantly increase the total value of your claim. We look for these discrepancies where general customs brokers often fail, ensuring that every dollar of overpaid duty is identified for recovery.

How to File Your Claim via the CAPE Tool and ACE System

Once you have isolated the high-value HTS codes from your import history, the focus shifts to the technical execution of your claim. Navigating the filing process for a Section 301 refund for automotive parts requires a precise interaction between your company's data and the Automated Commercial Environment (ACE). The launch of the Consolidated Administration and Processing of Entries (CAPE) tool in 2026 has streamlined what was once a disjointed protest process. This portal allows for the mass-submission of thousands of entries simultaneously, which is essential for automotive importers with complex, high-volume supply chains. Without this automated approach, the administrative burden of filing individual protests would likely exceed the value of the recovery itself.

Technical Requirements for the CAPE Portal

Uploading your specific list of entries into the CAPE portal triggers an automated CBP review designed to verify eligibility against current court mandates. The system is programmed to distinguish between the struck-down IEEPA duties and other valid tariffs that may still be owed, ensuring that your claim remains legally sound. If the system flags an entry for manual review, it typically indicates a discrepancy in the original duty calculation or a conflict with existing liquidation records. Resolving these flags quickly is paramount to keeping your recovery on track and avoiding lengthy administrative delays that could push your claim past the final filing window.

Managing the ACE Entry Summary Process

Effective recovery starts with a comprehensive data pull from the ACE system. You must extract at least five years of automotive import data to ensure no eligible entries are left behind. Distinguishing between liquidated and unliquidated entries is critical; liquidated entries often require a specific protest mechanism, while unliquidated entries may be adjusted through administrative corrections. You can see how it works for high-volume importers who need to process massive datasets without disrupting their daily operations. This data extraction must be exhaustive to capture every dollar of overpaid duty.

Validating your Entry Summaries (Form 7501) is the final layer of defense against claim rejection. Each form must be cross-referenced against your internal commercial records to ensure the duty paid matches the amount being reclaimed. Given the sheer volume of data involved in automotive manufacturing, mass-processing these entries is the only viable way to meet the strict April 2026 deadlines. Waiting until the final months of the eligibility period to begin this extraction will likely result in missed opportunities, as the system will inevitably become congested with last-minute filers seeking their own Section 301 refund for automotive parts.

Overcoming the Burden of Proof: Documentation Strategies

The burden of proof in any recovery action lies entirely on the importer. Customs and Border Protection (CBP) will not assist you in identifying overpayments; they require you to present a flawless evidentiary trail. The primary reason for claim rejection is insufficient evidence of duty payment, a hurdle that often trips up even the most organized logistics teams. To secure a Section 301 refund for automotive parts, you must move beyond simple spreadsheets. You need to prove that the "structural excess capacity" findings, which served as the legal justification for these tariffs, did not actually dictate the pricing or market conditions for your specific components. This requires a narrative that connects your financial records to the legal reality of the court's strike-down.

Organizing your documentation is a high-stakes endeavor. You must align commercial invoices, packing lists, and bills of lading with your ACE entry data. Any discrepancy, however minor, gives CBP a reason to deny your recovery. This is why a Tariff Eligibility Assessment is an essential prerequisite before filing. It ensures that your claim is grounded in verifiable data rather than assumptions. If you cannot provide a direct link between the duty paid and the specific HTS code being challenged, your capital will remain in the government's hands.

Critical Documents for Automotive Importers

Automotive supply chains involve thousands of sub-assemblies, making HTS classification rationales vital. You must be able to defend why a specific component was categorized under a List 3 or List 4a code. You will also need definitive proof of payment, typically via Customs Form 368 or equivalent financial records that show the 25% or 7.5% duties leaving your accounts. Many importers struggle with missing records from the 2018 to 2020 window. See our FAQ for common documentation hurdles and strategies to reconstruct your filing history when original files are incomplete.

Avoiding the "Audit Trap" During Recovery

Importers often fear that filing for a significant refund will trigger a broader customs audit. This fear is valid if your claim is poorly constructed or inconsistent with your historical filings. To protect your business, you must ensure total consistency across all past automotive import records. Professional verification of HTS codes is the primary defense against CBP inquiries. By presenting a clean, professionally audited claim, you signal to CBP that your compliance standards are elite, which actually reduces the likelihood of a disruptive audit. Don't leave your recovery to chance. Secure your customs documentation management audit today to ensure your files are bulletproof and ready for the April 2026 deadline.

Maximizing Recovery with Professional Contingency Advocacy

Reclaiming millions in overpaid duties isn't a task for generalists. While your customs broker manages daily logistics, they're rarely equipped for the forensic legal work required to secure a Section 301 refund for automotive parts. Specialized trade consultants bridge the gap between regulatory compliance and financial restoration. By leveraging experts who focus exclusively on IEEPA and Section 301 litigation, you ensure that every eligible entry is identified and correctly filed through the CAPE tool. This specialized advocacy is the difference between a partial recovery and reclaiming the full amount your business is legally owed.

We handle the heavy lifting of the entire filing process. Our team acts as your active engine for recovery, allowing your internal staff to focus on production and supply chain management. Positioning your business for the final 2026 filing window requires immediate action. The system will become increasingly congested as the April deadline approaches; therefore, securing a high-performing partner now is critical to avoiding administrative bottlenecks. Our team manages the complexities of the recovery process, including:

- Forensic auditing of five years of ACE import data.

- Automated mass-processing of entries via the CAPE portal.

- Direct communication with CBP to resolve flagged entries.

- Full documentation management to prevent audit triggers.

Contingency vs. Hourly Legal Fees

The most significant advantage of our model is the elimination of upfront financial risk. Many law firms charge high hourly rates regardless of the outcome, creating a barrier for mid-sized automotive firms. Our contingency-based approach aligns our incentives with yours: we only win when you recover your capital. This partnership model is built on transparency and results. Internal teams often miss 20% to 30% of eligible automotive entries because they lack the specialized auditing tools required for high-volume manufacturing data. By choosing contingency advocacy, you gain access to elite trade expertise without adding a single dollar to your overhead until your refund is secured.

Your Next Steps: The Eligibility Assessment

Your path to recovery begins with a zero-cost review of your automotive import history. This assessment quantifies your potential refund and identifies the specific HTS codes that qualify under the recent court rulings. Once we submit your claim via the CAPE tool, the timeline for recovery depends on CBP processing speeds, but our managed filing ensures your entries are at the front of the queue. For automotive executives who need to understand the underlying legal mechanics, we provide a detailed look at how IEEPA explained functions within the context of manufacturing duties. Don't let the 2026 window close on your capital. Start your assessment today to secure your Section 301 refund for automotive parts and reclaim what the government shouldn't have taken.

Secure Your Automotive Duty Restoration Today

The landscape of trade has shifted in your favor, but the clock is ticking on your ability to reclaim overpaid capital. You've identified the high-value HTS codes and understood the technical requirements of the ACE system; now, you must execute your claim with precision. Successfully securing your Section 301 refund for automotive parts requires more than just submitting data. It demands a bulletproof documentation strategy and the specialized advocacy to navigate the 2026 CAPE tool filing process without triggering a disruptive audit.

We take on the full management of your claim, removing the financial barriers and administrative heavy lifting that often stall recovery efforts. With our contingency-based model, there are no upfront costs. Our deep expertise in IEEPA and Section 301 automotive claims ensures your business is positioned for maximum restoration. Don't let your capital remain in the government's accounts when the law now recognizes your right to its return. Take the first step toward reclaiming your millions today and let us handle the rest of the bureaucracy for you.

Get Your Free Automotive Tariff Eligibility Assessment Now

The window to act closes in April 2026. We're ready to win back your overpaid duties with the professional confidence your bottom line deserves.

Frequently Asked Questions

Is the Section 301 refund for automotive parts real or a scam?

The Section 301 refund for automotive parts is a legitimate legal recovery based on federal court rulings that struck down specific IEEPA duties. This is not a speculative opportunity; it's a court-ordered restoration of capital that was collected without proper statutory authority. Automotive importers have a valid pathway to reclaim these funds, provided they meet the strict documentation and filing requirements set by CBP for the 2026 recovery window.

How far back can I go to claim refunds on automotive imports?

You can typically recover duties on entries dating back to the peak tariff period of 2018 through 2020. Your eligibility depends on whether these entries were subjected to List 3 or List 4a duties and if they haven't passed the final liquidation protest window. Auditing your five-year import history is the only way to ensure that no high-value entries are left behind as the statute of limitations approaches.

What is the deadline for filing a Section 301 or IEEPA refund claim in 2026?

The primary deadline for filing your Section 301 refund for automotive parts claim is April 2026. This date is the final cutoff for entries affected by the landmark IEEPA litigation and the subsequent strike-down of expanded duties. If you fail to file before this window closes, your entries will be permanently liquidated. This means the government will keep your overpaid capital forever, regardless of the legal merits of your case.

Can I claim a refund if my automotive parts were on List 4a?

Yes, automotive parts on List 4a are eligible for recovery if they were part of the expanded duties that the courts determined were unauthorized. While List 3 carried a higher 25% duty rate, the 7.5% duties applied to List 4a components still represent a significant financial burden for high-volume importers. Every entry summary should be audited to ensure you aren't leaving this capital on the table.

What is the CAPE tool and do I need it for my claim?

The Consolidated Administration and Processing of Entries (CAPE) tool is the mandatory portal for mass-filing these specific recovery claims in 2026. You need it to process thousands of entries efficiently and ensure they're recognized by CBP's automated review system. Without this tool, the administrative burden of filing individual protests for a complex automotive supply chain would be nearly impossible for most businesses to manage.

How long does it take for CBP to process an automotive tariff refund?

Processing times typically range from six to twelve months after a successful CAPE submission, depending on the complexity of your import data. CBP's automated systems have streamlined the initial verification, but manual reviews of flagged entries can extend the timeline. Filing early in the 2026 window is the best strategy to avoid the massive congestion expected as the final April deadline draws near.

Do I need a lawyer to file for a Section 301 refund?

While a lawyer isn't strictly required, the technical complexity of these claims makes professional trade advocacy essential for a successful recovery. Specialized trade consultants often provide a more efficient, data-driven path than general legal counsel by focusing on the ACE data extraction and documentation management. Our contingency model ensures you have expert representation without the burden of upfront hourly legal fees or financial risk.

What happens if my automotive parts were misclassified in the past?

Misclassified parts remain eligible for recovery if the corrected HTS code falls under the struck-down legal authority. Our team identifies these errors through a comprehensive tariff eligibility assessment, ensuring that your claim reflects the accurate classification of your components. Correcting these past mistakes often uncovers hidden recovery opportunities while simultaneously hardening your compliance records against future CBP audits or inquiries.

Ready to find out what your business may be owed?

Check My Eligibility