The section 301 tariff refund deadline you've been monitoring is likely a distraction from the real financial recovery window closing right now. While many importers are fixated on the latest 2026 exclusion dates, the true urgency lies in the wake of the Supreme Court's February ruling that invalidated IEEPA-based duties. You've likely spent years overpaying for imports while struggling to keep pace with shifting trade policies, and the fear of missing a multi-million dollar recovery window is a legitimate business concern. It's exhausting to navigate a system that feels designed to keep your capital in government hands.

This article provides the professional clarity you need by distinguishing between Section 301 timelines and the critical IEEPA statute of limitations. You'll discover the exact dates that matter for your 2026 filings and learn how to determine if your specific imports qualify for a significant refund. We'll strip away the confusion surrounding customs documentation and provide a low-risk strategy to initiate your claim before these legal windows shut for good. With the June 2026 appeal of the IEEPA refund order creating fresh uncertainty, the time to identify your eligibility is today, not after the next regulatory shift.

Key Takeaways

- Understand why the section 301 tariff refund deadline is often misunderstood and how the 2026 Supreme Court ruling actually redefined your window for recovery.

- Learn how the IEEPA exception allows your business to reclaim overpaid duties even if you missed the standard 180-day CBP protest window.

- Debunk the common myths that prevent importers from pursuing millions in refunds, including dangerous misconceptions about customs broker oversight.

- Discover the specific two-step audit process for your 7501 forms to identify if your firm qualifies for a major financial restoration.

- Evaluate the advantages of a contingency-based recovery model that eliminates upfront costs and shifts the legal risk away from your balance sheet.

The Truth About the Section 301 Tariff Refund Deadline

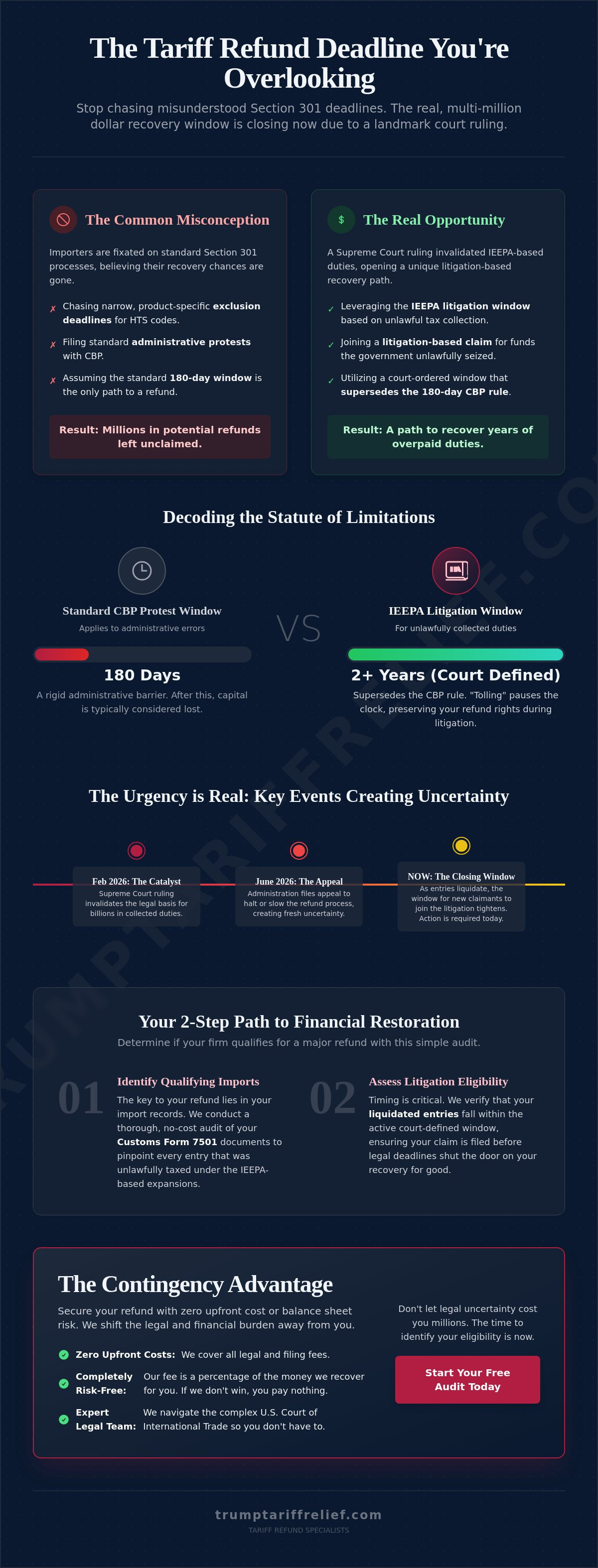

Most importers are currently chasing a section 301 tariff refund deadline that doesn't exist in the way they think. They spend hours searching for exclusion windows, yet the real opportunity for a multi-million dollar recovery stems from the International Emergency Economic Powers Act (IEEPA). The landscape shifted dramatically following the February 2026 Supreme Court ruling. This decision didn't just offer a new perspective; it invalidated the legal basis for billions in collected duties. If you've been waiting for a sign to audit your trade expenses, this ruling is the definitive catalyst.

2026 has become the "Year of Recovery" for U.S. importers who recognize the distinction between a standard administrative protest and a litigation-based claim. A protest is a routine challenge to a specific entry's classification or valuation. A litigation-based claim is an assertive demand for the return of funds based on the court's finding of unlawful government action. You aren't just asking for a favor; you're reclaiming capital that was seized under a legal framework the highest court has now rejected. For businesses that acted quickly after the February ruling, the path to restoration is already moving through the federal system.

Section 301 vs. IEEPA: Which Deadline Matters?

To understand your path forward, you must look at the history of Section 301 of the Trade Act of 1974. While Section 301 governs the specific tariffs on Chinese goods, the method the government used to expand those tariffs often relied on IEEPA. Standard Section 301 exclusion periods are narrow and product-specific. If you missed a deadline for a specific HTS code exclusion, you might assume your chance for a refund is gone. That's a costly mistake. The IEEPA-based recovery path operates on a different timeline, focusing on the illegality of the tax itself rather than the specifics of the product. You can find a deeper breakdown of this distinction in our guide on how IEEPA recovery works.

The Role of the U.S. Court of International Trade (CIT)

The U.S. Court of International Trade (CIT) is the engine behind these payouts. CIT orders dictate when the government must release funds, and these timelines are shifting in real-time. For example, the Trump Administration filed a critical appeal on June 2, 2026, attempting to halt or slow the refund process. This creates a high-stakes environment where the status of your "liquidated entries" determines your eligibility. Liquidated entries are those that Customs has finalized; once this happens, the clock starts ticking on your ability to join the litigation. The CIT's recent activity, including the public comment periods earlier this year, suggests that the window for new claimants is tightening. If your entries are liquidating now, you don't have the luxury of waiting for the next quarterly report to take action.

Decoding the Statute of Limitations: 180 Days vs. The Court Window

Most importers operate under the assumption that once 180 days pass after entry liquidation, their capital is permanently lost to the government. This is the standard U.S. Customs and Border Protection (CBP) protest window. It's a rigid administrative barrier designed to finalize revenue and prevent long-term liability for the Treasury. However, the current litigation landscape has shattered this traditional boundary. If you're currently searching for a section 301 tariff refund deadline, you must understand that the IEEPA ruling operates on a parallel track that ignores these standard limitations.

The standard 180-day rule only applies to administrative errors or classification disputes. Recent court rulings on tariff legality have established that the duties collected under the 2024-2026 expansion were fundamentally unlawful. When a tax is found to be illegal from its inception, the court window often supersedes the CBP window. This creates a powerful exception for businesses that previously thought they were "out of time." You aren't just filing a protest; you're joining a federal litigation effort to recover funds that the government had no right to collect in the first place.

Tolling the statute of limitations is the most critical concept for your recovery strategy. Tolling essentially pauses the clock, preserving your right to a refund while the appellate courts finalize the payout structure. Waiting for "final clarification" from the government is a tactical error that often leads to permanent financial loss. Every shipment that liquidates without a pending claim is a shipment that might fall outside the court's protection. It's the most expensive mistake a CFO can make in 2026. You can see exactly how we manage these high-stakes timelines by reviewing how it works for our partners.

Understanding Entry Liquidation Dates

Liquidation is the "ticking clock" of customs law. It's the date CBP officially finalizes the duty amount for an entry. This usually happens 314 days after the date of entry, but you can track the exact status in your ACE portal. Be particularly wary of "deemed liquidated" entries. These occur automatically if CBP fails to act within one year. Even if an entry is deemed liquidated, it remains eligible for IEEPA recovery if you act before the court-mandated window closes.

Retroactive Claims: How Far Back Can You Go?

The Supreme Court's February 2026 decision has effectively reopened windows for entries dating back to late 2024. Because the litigation challenges the very authority of the IEEPA expansion, the lookback period is surprisingly broad. We are currently auditing 7501 forms for the entire 2024-2026 tariff period to identify every eligible dollar. If you paid duties on Chinese imports during this window, there's a strong probability that those funds are currently sitting in a government account waiting for a valid claim.

Myth vs. Reality: Reclaiming Your China Tariff Payments

The government is not your financial advisor. It's a revenue-driven bureaucracy that has no legal obligation to notify your firm of its eligibility for a refund. If you're waiting for a letter from Customs explaining the section 301 tariff refund deadline, you're essentially forfeiting your capital. The reality of trade recovery is that the burden of discovery and assertion lies entirely on the importer. Most businesses operate under a cloud of misinformation that prevents them from reclaiming what is rightfully theirs.

One of the most persistent myths is that Section 301 and IEEPA are interchangeable terms. They are not. Section 301 provides the authority for the trade actions against China, but the International Emergency Economic Powers Act (IEEPA) was the specific mechanism used to expand those duties in ways the courts have now deemed unlawful. If you focus solely on Section 301 exclusion lists, you're looking at a narrow sliver of the potential recovery. The real financial restoration comes from the IEEPA-based claims that bypass standard product-specific exclusions. This distinction is the primary reason why so many companies leave millions of dollars on the table; they're looking for the wrong deadline in the wrong regulatory framework.

Why Brokers Often Miss the Recovery Window

Many executives believe their customs broker would have flagged this opportunity. This is a dangerous assumption. Brokers are experts in the current flow of goods; they prioritize clearance, compliance, and velocity for today's shipments. They are rarely equipped or incentivized to manage historical recovery litigation that requires a deep audit of settled entries. Administrative filing and legal recovery litigation are two entirely different disciplines. Trump Tariff Relief acts as a specialized layer of expertise that complements your existing team. We handle the heavy lifting of the audit and legal assertion without disrupting your daily logistics operations.

Is the China Tariff Refund Real?

The legitimacy of this recovery effort is backed by the highest legal precedents in the country. The February 2026 Supreme Court ruling wasn't just a suggestion; it was a mandate that invalidated the legal foundation of these specific expanded duties. Even the Trump Administration's June 2, 2026, appeal of the refund order confirms the high stakes of this battle; the government is fighting to keep the funds because they know the legal ground has shifted. For a granular look at the legal framework and how it applies to your specific HTS codes, visit our IEEPA Explained page. This is not a speculative "maybe" situation. It's a structured legal process with a defined, albeit closing, window for participation.

How to Calculate Your Firm’s Final Filing Deadline

Calculating your specific section 301 tariff refund deadline isn't a matter of checking a public calendar; it's a forensic exercise in customs data analysis. Your deadline is uniquely tied to the date your goods cleared the port and when those entries were finalized by CBP. Most importers make the mistake of waiting for a industry-wide notification that never comes. Instead, you must work backward from your entry liquidation dates to ensure your claim is filed while the court window remains open. This process requires a level of precision that standard logistics providers simply aren't equipped to handle.

To secure your recovery, follow this assertive five-step protocol:

- Step 1: Audit your 7501 Entry Summaries for the last 24 months. You need a complete dataset to identify every eligible transaction.

- Step 2: Identify the specific "Duty Code" used for your China imports. You're looking for the additional duties tied to the 2024-2026 expansion.

- Step 3: Cross-reference your liquidation dates with the IEEPA ruling timeline. If an entry liquidated within the last 180 days, your priority is high.

- Step 4: Assess the "Summons and Complaint" status for your specific HTS codes. This legal step is what preserves your right to the refund.

- Step 5: Secure expert filing before the next Court of International Trade (CIT) cutoff. The June 2026 appeal by the administration has made these windows more volatile.

The Essential Documentation Audit

Your recovery lives or dies by your documentation. You must gather every Entry Summary and Commercial Invoice related to your China-origin shipments. HTS codes are the primary filter here; they determine your position in the litigation queue and your specific deadline priority. Digital record-keeping is your best ally in this stage. If your records are fragmented across multiple brokers or physical files, you're at a significant disadvantage. We use these documents to build a bulletproof case for your IEEPA recovery, ensuring no dollar is left behind due to clerical oversight.

Identifying "High-Risk" Deadlines

Certain sectors are under more pressure than others. Electronics, Machinery, and Textiles face the earliest cutoffs because they represent the bulk of the contested duties. If your business operates in these industries, you must prioritize entries approaching the 180-day mark. Your customs broker is a logistics partner, not a litigation specialist, and they often miss these windows because they aren't tracking the CIT's moving targets. Don't leave your capital to chance. You can request a free eligibility assessment right now to see your firm's specific timeline and potential recovery amount before the next regulatory shift occurs.

The Contingency Advantage: Securing Your Refund with Zero Upfront Cost

The most significant barrier to entry for many importers is the perceived cost of litigation. Traditional law firms often operate on hourly billing models that require a massive capital outlay before a single dollar is recovered. In a landscape where the government is actively fighting to retain your funds, as evidenced by the June 2, 2026, appeal of the CIT's refund order, paying upfront for a "maybe" is a high-risk gamble. The contingency model is the only logical choice for businesses that want to protect their bottom line while pursuing a section 301 tariff refund deadline recovery. It shifts the entire financial burden from your balance sheet to our expertise.

Trump Tariff Relief operates on a "No-Win, No-Fee" promise. This aligns our success directly with your financial restoration. We take the legal and administrative risk, providing you with a high-reward partnership that requires no initial investment. If we don't recover your overpaid duties, you don't owe us a cent. This assertive approach ensures that your business can join the multi-billion dollar litigation effort without diverting resources from your core operations. We act as your powerful ally, righting the wrong of unlawful taxation with professional confidence.

Our Process: From Documentation to Deposit

Our recovery engine is designed for speed and precision. We handle the entire summons and complaint process, moving your claim through the Court of International Trade with surgical efficiency. Once we complete your initial IEEPA Tariff Refund Recovery assessment, we take over the heavy lifting. This includes managing complex customs documentation and navigating the specific CIT filing requirements that general legal counsel often overlooks. Our specialized focus on IEEPA-based claims allows us to outperform generalists who don't have the deep, technical knowledge of the 2024-2026 tariff expansions. You can expect a streamlined path from the initial audit to the final deposit of your recovered capital, with regular updates as the litigation progresses. Learn more about how it works to see the momentum we build for our partners.

Final Call to Action: Protect Your Capital

The cost of inaction is absolute. Once the section 301 tariff refund deadline and the accompanying IEEPA windows pass, your overpaid duties stay with the U.S. Treasury permanently. The government won't offer a second chance to claim these funds. Thousands of U.S. businesses are already reclaiming their capital, and your firm shouldn't be the exception. Don't let bureaucracy win by default. Visit our FAQ for immediate answers to common deadline questions, or contact us today to secure your place in the recovery queue. The window is closing, and the time to act is now.

Secure Your Financial Restoration and Protect Your Bottom Line

The window for reclaiming your overpaid duties is narrow and closing fast. You've learned that the 2026 Supreme Court ruling has fundamentally changed the rules of engagement, making the distinction between IEEPA and Section 301 the most critical factor in your recovery strategy. Focusing on the wrong section 301 tariff refund deadline could cost your firm millions in lost capital that rightfully belongs on your balance sheet. The government isn't going to volunteer this money back; it requires an assertive, legal-based claim.

We are prepared to act as your sophisticated advocate, providing expert navigation of the current litigation landscape and managing everything from the initial audit to final documentation. We take on the legal risk so you don't have to. With our contingency-based model, you only pay if we recover your money. It's a professional partnership designed to restore your financial health without any upfront burden. You've paid the price of trade uncertainty long enough; it's time to reclaim your capital and right this financial wrong.

Start Your Free Tariff Eligibility Assessment Now. Take the first step toward securing the recovery your business deserves today.

Frequently Asked Questions

Is there a specific date for the Section 301 tariff refund deadline in 2026?

There is no single universal date for the section 301 tariff refund deadline in 2026. Instead, your filing deadline is determined by the liquidation dates of your specific entries and the lookback windows established by the Court of International Trade. While July 6, 2026, is a critical date for public comments on new trade actions, the window for past recovery is a separate legal track that requires immediate assertion to preserve your rights.

Can I still get a refund if my entries have already liquidated?

You can absolutely secure a refund even if your entries have already liquidated. In fact, liquidated entries are the primary focus of the IEEPA recovery process. Once an entry liquidates, the clock begins for standard administrative protests, but the current litigation path allows us to challenge the legality of the duty itself for entries dating back to 2024. This bypasses the typical finality that usually accompanies the liquidation process.

What is the difference between a CBP protest and an IEEPA litigation claim?

A CBP protest is a routine administrative challenge filed directly with Customs within 180 days of entry liquidation. An IEEPA litigation claim is a more powerful legal action filed in the U.S. Court of International Trade. While a protest typically handles clerical or classification errors, an IEEPA claim challenges the fundamental authority of the government to collect expanded tariffs that the courts have recently deemed unlawful.

How far back can I claim refunds for China tariffs?

You can typically claim refunds for entries dating back to late 2024. The February 2026 Supreme Court ruling opened a lookback window that covers the specific period when the IEEPA-based expansions were in effect. We audit your 7501 forms for the entire 2024 to 2026 period to ensure that every eligible dollar is included in your summons and complaint before the court-mandated windows close.

Does my company need a lawyer to file for these tariff refunds?

Your company requires specialized legal representation because these are litigation-based claims, not simple administrative filings. These actions must be filed in the U.S. Court of International Trade to be valid. We manage this entire process for you, handling the heavy lifting of the audit and the summons and complaint so your team can focus on operations while we pursue your financial restoration.

What happens if I miss the 180-day protest window?

Missing the 180-day protest window doesn't necessarily end your chance for recovery. The IEEPA litigation track provides a separate path for entries that are technically final in the eyes of CBP but still subject to the court's ruling on unlawful taxation. If your entries fall within the court's lookback period, you can still join the litigation effort despite missing the standard administrative protest deadline.

How long does the actual refund process take once a claim is filed?

The timeline for payouts is currently influenced by the government's June 2, 2026, appeal of the CIT refund order. While the filing process happens quickly, the actual deposit depends on the court's final distribution schedule. By filing now, you ensure your firm is in the first wave of recipients once the appellate court clears the path for the government to release these contested funds.

Are all Section 301 tariffs being refunded following the Supreme Court ruling?

Only specific expanded duties are eligible for refund following the Supreme Court ruling. The court found that certain global surcharges and expansions exceeded the government's authority under IEEPA. Standard Section 301 duties on original product lists may still apply. We provide a Tariff Eligibility Assessment to identify exactly which of your China imports qualify for a significant financial recovery.

Ready to find out what your business may be owed?

Check My Eligibility